As AI data centers expand rapidly, optical modules and optical chips are becoming one of the most important bottlenecks in the AI infrastructure supply chain.

Memory stocks have been soaring.

Have you gotten in yet?

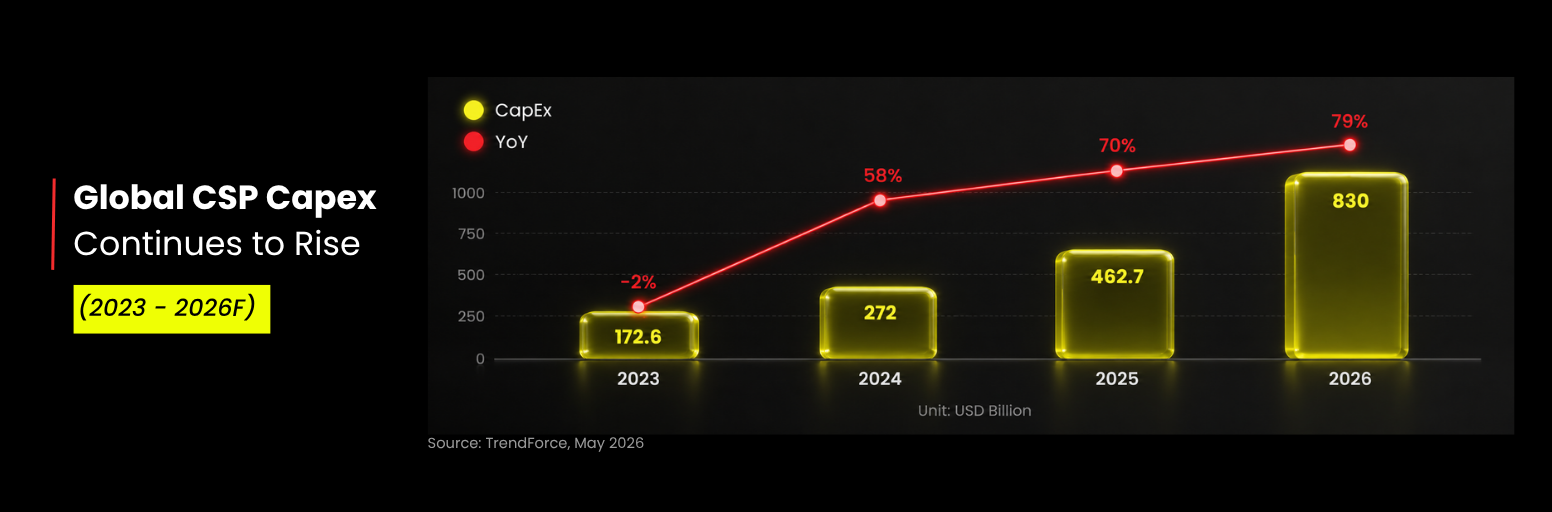

AI infrastructure spending continues to accelerate, with no signs of slowing down. Earnings reports from Microsoft, Google, Amazon, and Meta show that major cloud service providers continue to aggressively increase capital expenditure.

Google even revealed that the backlog of its cloud business nearly doubled from the previous quarter. Management admitted that growth could have been even stronger if not for shortages in AI hardware supply. Other major cloud players have also expressed strong confidence in the resilience of current AI demand.

At the same time, memory stocks have already experienced massive rallies. Micron Technology, for example, pulled back from a peak of around $818.67 to roughly $700, highlighting growing valuation concerns across the memory sector.

The AI infrastructure cycle is still in full swing.

But investors are now asking a new question:

What comes after memory stocks?

One answer may be optical modules and the broader optical communication supply chain.

1. AI Computing Demand Is Driving Optical Module Growth

The market initially focused almost entirely on computing power.

Then it discovered memory.

Now, another bottleneck is becoming increasingly important:

data transmission speed.

AI Needs More Than Computing Power

Imagine a person with Einstein-level intelligence but terrible memory.

He solves the problem, then instantly forgets it.

No matter how intelligent he is, his performance slows dramatically.

That is essentially what happened with AI infrastructure.

The industry realized that memory chips were critical for supporting AI workloads.

But computing power and memory alone are not enough.

The “nervous system” matters too.

If someone touches a hot stove and only reacts five seconds later, the issue is no longer intelligence. The issue is transmission speed.

That is now becoming one of the biggest challenges for AI infrastructure.

Why Optical Modules Matter

As AI models continue expanding, computing workloads grow exponentially.

That means:

- more data transfer

- higher bandwidth demand

- greater power consumption

Traditional copper cables are increasingly struggling to keep up.

As electrical signals travel through copper, large amounts of energy are lost as heat due to resistance. At AI scale, this becomes highly inefficient.

Light is simply faster and more efficient.

That is why optical communication is becoming essential for next-generation AI data centers.

Optical modules are key components that convert optical signals into electrical signals and vice versa. They are critical for:

- AI data centers

- cloud computing infrastructure

- telecom networks

- high-performance computing systems

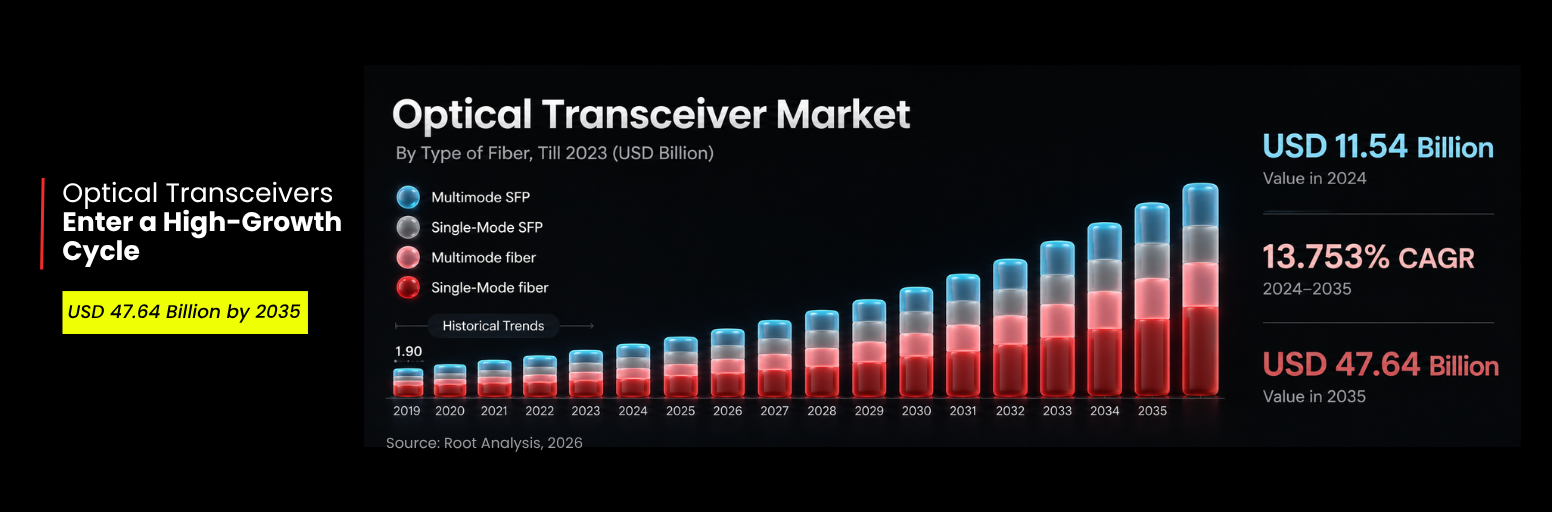

A Massive Growth Market

The global optical module market was valued at USD 11.54 billion in 2024 and is expected to reach USD 47.64 billion by 2035, with a compound annual growth rate of around 13.75%.

The AI data center market itself is expected to grow even faster.

According to Precedence Research:

- AI data center market (2025): USD 17.54 billion

- AI data center market (2034): USD 165.73 billion

This represents nearly a 10x expansion in less than a decade.

2. Why AI Data Centers Need Optical Communication

AI infrastructure consumes enormous amounts of electricity.

By 2030, global data center power consumption is expected to rise from around:

- 30 GW today

to more than

- 90 GW

That is a threefold increase.

The Real Bottleneck: Data Transmission

As AI model parameters expand, the computing workload for a single task increases exponentially.

More importantly, the industry still believes current AI systems are far from reaching true intelligence. Engineers continue pursuing larger and more powerful systems, with some future AI racks potentially targeting:

- 1 megawatt per single rack

At that scale, traditional copper infrastructure becomes insufficient.

This is where optical communication becomes critical.

The Role of EML Chips

One of the most important components inside optical modules is the EML chip (electro-absorption modulated laser).

These chips generate the high-speed laser signals required for data transmission.

Current 800G optical modules typically require:

- 8 EML chips per module

A single high-performance switch may contain:

- 64 ports

That means one switch alone can consume:

- 512 EML chips

And an AI data center equipped with 100 such switches would require more than:

- 50,000 EML chips

Demand Is Exploding

Demand for 800G and higher-speed optical modules is expected to rise sharply:

- 2025: 24 million units

- 2026: nearly 63 million units

This translates into annual demand for roughly:

- 200 million to 500 million EML chips globally

The scale of this industry is becoming enormous.

3. Where Is the Real Value in the Industry Chain?

The market already recognizes the importance of optical modules.

But not every part of the industry chain offers the same investment value.

The highest barriers and strongest pricing power remain concentrated upstream.

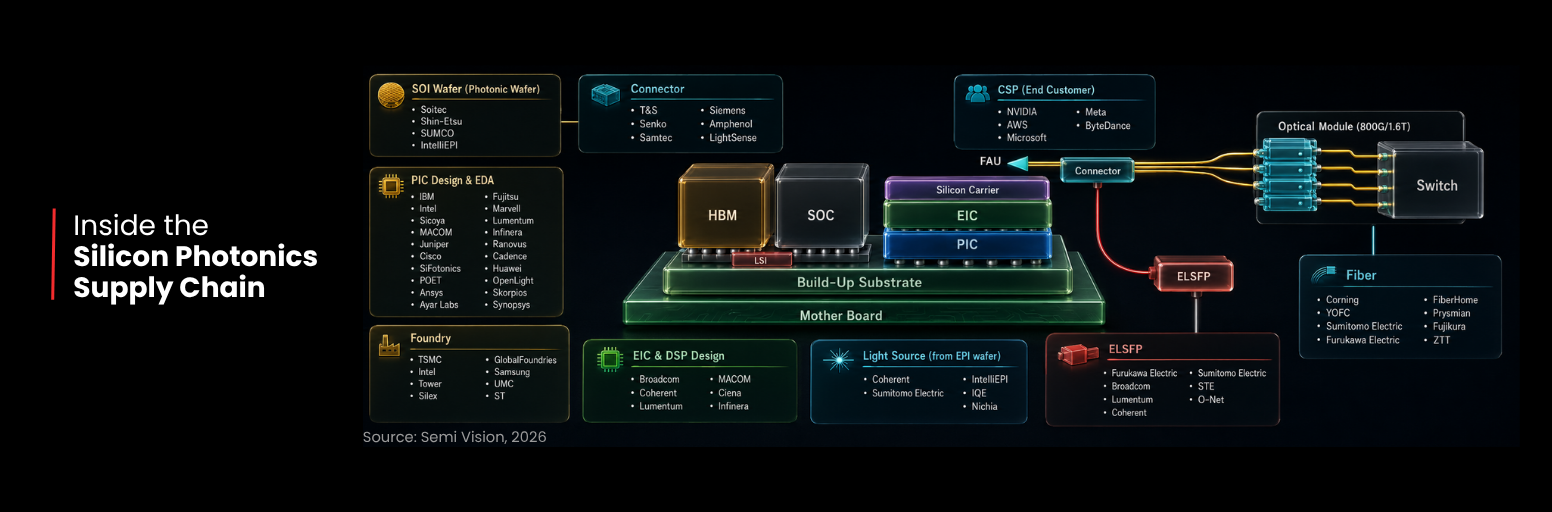

The Most Valuable Segment: Optical Chips

The upstream optical module supply chain includes:

- optical components

- optical and electrical chips

- packaging materials

- production equipment

Among these, optical chips are the most critical.

Different Types of Optical Chips

Optical chips are mainly divided into:

- Indium phosphide (InP)

- Gallium arsenide (GaAs)

- Silicon photonics

Each serves different communication requirements.

- InP → long-distance, high-speed communication

- GaAs → short-distance transmission

- Silicon photonics → large-scale integration using CMOS processes

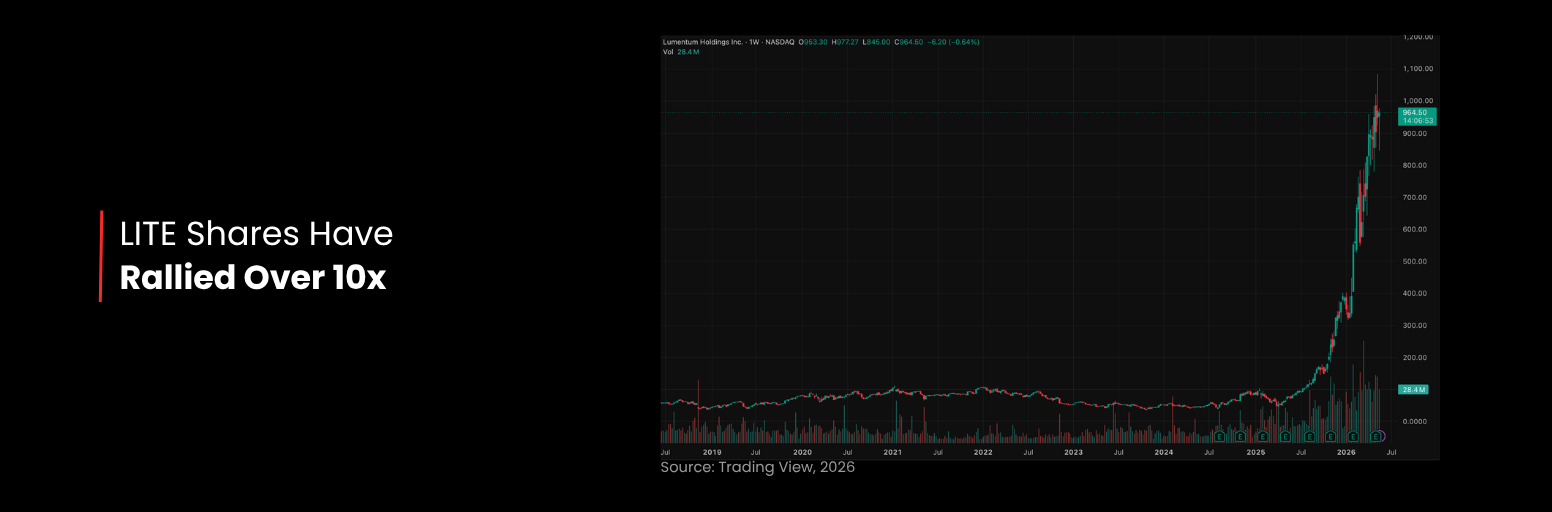

Lumentum remains one of the global leaders in high-end InP lasers and integrated optical systems, supported by strong IDM capabilities across chip design, wafer manufacturing, packaging, testing, optical modules, and optical switching solutions.

However, after a massive rally, investors are increasingly asking:

Where are the next opportunities beyond optical chips?

4. The Opportunity May Shift Toward Equipment

When capital crowds into one segment, opportunities often emerge elsewhere.

And right now, equipment may be the next area worth watching.

The Industry Is Undergoing Structural Change

Optical module manufacturing is evolving rapidly.

The industry is shifting from:

- traditional plug-in designs

toward:

- co-packaged optics (CPO)

- silicon photonic integration

At the same time, production lines are becoming increasingly automated and intelligent.

That means equipment standards are rising rapidly.

Precision Is Becoming Everything

Take the mounting process as an example.

Tiny optical and electrical chips smaller than a fingernail must now be placed with extreme precision.

Required accuracy has improved from:

- 10 microns previously

to around

- 3 microns today

That is only a fraction of the diameter of a human hair.

The chips are also extremely fragile.

Excessive force or poor temperature control can easily damage them, making precise force application and temperature management critical technical challenges.

Global leaders in this segment include:

- FOUR TECHNOS

- MRSI

- ASMPT

Bonding and Coupling Are Also Becoming More Complex

After mounting comes the bonding process, which uses ultra-thin gold wires to connect chips for signal transmission.

This process previously relied heavily on manual work, but increasing manufacturing standards now require far higher levels of precision and cleanliness.

Even microscopic impurities can affect signal quality and transmission speed.

Besi remains one of the global leaders in bonding equipment.

Coupling and Testing Are Emerging Bottlenecks

Coupling is one of the most time-consuming processes in optical module manufacturing.

A position offset of just:

- 1 μm

can result in:

- up to 3 dB of optical loss

As precision requirements continue rising, demand for advanced coupling systems is increasing rapidly.

ficonTEC remains one of the major global players in this segment.

Testing is also becoming increasingly difficult.

As network speeds move toward:

- 800G

- 1.6T

testing systems require extremely high bandwidth and advanced algorithms to capture tiny signal fluctuations.

Keysight and Anritsu currently dominate this market, with the top two players holding roughly:

- 53% combined market share

AI is the biggest opportunity of this era. Companies with true core competitiveness will ultimately survive and thrive through market cycles.

What This Means for Investors

The AI infrastructure cycle is no longer just about GPUs and memory.

The next wave may increasingly focus on:

- optical communication

- optical chips

- photonics

- precision manufacturing equipment

As AI systems become larger and more power intensive, data transmission efficiency becomes just as important as raw computing power.

Final Insight

The market spent the past year chasing AI computing power.

Then it discovered memory.

Now, another bottleneck is emerging:

the speed at which data moves.

And in the AI era, the companies controlling that “nervous system” may become some of the most important players in the entire industry.

Disclaimer

The information contained herein is provided for general informational and educational purposes only and does not constitute investment advice, financial advice, trading advice or any other form of professional advice, a recommendation, or an offer or solicitation to buy or sell any financial instruments or engage in any trading strategy.

Trading in leveraged products such as contracts for difference (CFDs) involves a significant risk of loss and may not be suitable for all investors. Past performance is not indicative of future results. Any references to market trends, asset performance, price levels, or forward-looking statements reflect opinions or general market commentary as at the date of publication and are subject to change without notice.

This article does not take into account any individual investor’s objectives, financial situation, or risk tolerance. Readers should conduct their own independent research and seek professional advice before making any investment or trading decisions. D Prime and its affiliates make no representations or warranties about the accuracy or completeness or reliability of this information and disclaim any and all liability for any direct, indirect, incidental, consequential, or other losses or damages arising out of or in connection with the use of or reliance on any information contained herein. The above information should not be used or considered as the basis for any trading decisions or as an invitation to engage in any transaction. Do not rely on this article to replace your independent judgment.

“D Prime” is a brand name of D Prime Vanuatu Limited, a company incorporated and regulated by the Vanuatu Financial Services Commission (Company Number: 700238). The availability of products and services may vary depending on jurisdiction and applicable regulatory requirements.